For years, the United States has been known worldwide for its massive issues regarding student loan debts. To put things into perspective, student loan debt statistics indicate that in the US, student debt has taken the second spot on the list containing the highest forms of consumer debt, thus surpassing automobile and credit card debt.

Because of this, hundreds of thousands of potential students choose not to pursue higher education, since the high cost would likely make many of them bankrupt. Many advocates believe that the situation isn’t directly linked to student debt, but rather to the tuition crisis present in numerous colleges throughout the US — and that’s a student loan debt fact. Lower tuition would make most of the country’s universities unsustainable, because of their large yearly spending. Government-based tuition would solve the issue as it does in all countries with a universal education ecosystem, yet most colleges are private, rather than state-owned, thus contributing to the challenge.

This article is meant to paint a clearer picture of the US higher education system, thus focusing on student loans and their impact on the individual.

5 Key Student Loan Debt Statistics in 2021 (Editor’s Pick)

[post_snippet]

Average College Debt in the US (2010–2021)

The number of students who owe at least $100,000 has risen to around 2.5 million- nearly 6% of the borrowing pool.

The typical student who borrows money to cover educational costs has an average debt of $17,000. The number of those who owe at least $100,000 has risen to 2.5 million - almost 6% of the entire borrowing pool, as per the Education Department data.

The government allows students to borrow almost any amount they need to cover educational costs, like living expenses and tuition, without much guidance on repayments. Universities have little incentive to change things and rising student loan debt has become a serious issue.

An estimated 35 million Americans may qualify for student debt relief under the CARES Act of 2020.

The CARES act covers Federal student loans that are owned by the US Department of Education while loans that are not federally owned or private student loans are not covered. The CARES Act offered student loan debt relief affecting at least 20 million borrowers by the end of the third quarter of 2020.

In early 2020, 75.3% of private student loans were in repayment while 20% were in deferment.

The student loan market is filled with many private lenders who often provide suspension in payments for up to 3 months. Private student loans in deferment accounted for 20% of all private student loans in early 2020, while 75.3% were in repayment.

The percentage of applications that are rejected every year is steadily rising.

Partial or complete student loan debt forgiveness may be possible for borrowers under certain conditions. Most borrowers are unaware that they are eligible and qualify for student loan debt forgiveness.

Only a surprising 6.7% of borrowers who are eligible apply for loan forgiveness and the federal government forgives at a default rate on student loans of $95.45 per indebted borrower. Still, the percentage of student debt forgiveness applications that are rejected each year is steadily rising.

Students obtaining higher degrees have the tendency to take loans, but they usually pay them off on time.

This is certainly the case because, on average, the weekly earnings for those with a bachelor's degree is almost twice that of those with high school diplomas. Similarly, the student debt by major may vary, but investing in quality higher education correlates with higher earnings.

This results in people with advanced degrees accumulating more debt but being more likely to make timely payments due to their relatively higher earnings.

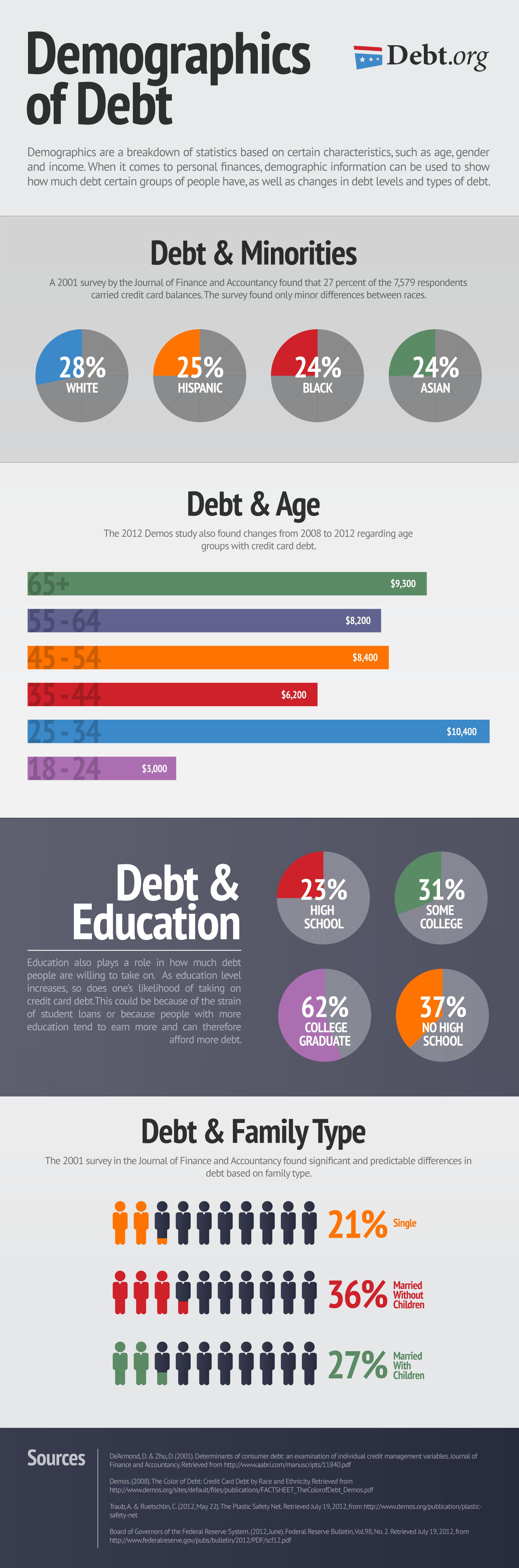

African American college students are the most likely to use federal loans, with 49.4% borrowing, while Asian students (at 62%) are the least likely to receive federal loans.

The student loan debt by race statistics indicates that white students are more likely to receive private loans with 7.1% borrowing privately whereas African American students are most likely to use federal loans. Almost half of all African American college students borrow federal loans while Asian students are least likely to receive federal loans.

At least 48% of African American students owe an average of 12.5% more than they borrowed just 4 years after graduation and 30% of African American graduates default in the first 12 years of repayment.

According to the Federal Reserve, it seems like the average debt for students was approximated at $25,000 in 2017

Keep in mind that this statistic is based on data concerning all individuals who still have student debt at this point in time, meaning it includes those who have already been making payments for a while. The actual average debt for graduating students is much higher, as US student loan debt data points out.

Source: Federal Reserve

A research study has determined that $29,800 was the average debt for students graduating in 2018

In time, these numbers have fluctuated quite a bit, as we will see later on. It’s important to remember that having this much outstanding payments between the ages of 21–25, makes it considerably more difficult to pay the debt, given the low entry-level salaries.

Source: Student Loan Hero

According to student loan debt statistics, debt was estimated at $0.76 trillion in the first quarter of 2010 and $1.46 trillion in the fourth quarter of 2018

Hence, we can clearly see that the problem is only getting worse. This is directly linked to increased spending in private colleges, alongside the lack of government action on the matter.

Source: NBC News

Over 25% of borrowers owe between $10,000 and $25,000 in student debt

Graduating doesn’t ensure a high-paying job. Rather, many college graduates end up being unemployed for a long while, whereas others continue to work minimum wage jobs. Paying debt is also difficult due to the lack of well-paying opportunities for new graduates, as indicated by student debt statistics.

Source: NBC News

It looks like just 20% of students affected by debt are close to paying off their remaining debt

Therefore, according to these stats, around 18% of US college students owe between $1 and $5,000, which can be paid off much faster when compared to those owing above $25,000, as pointed out by statistics concerning the average student loan debt.

Source: NBC News

Less than 10% of college students owe between $50,000 and $75,000 worth of debt, whereas less than 10% owe between $75,000 and $200,000+

In the case of graduates who finish their degrees in costly universities, statistics point out that there are roughly 18% who owe over $50,000 in debt. Higher debt usually entails a more expensive university, which likely offers better programs. This means that students are more likely to get better-paying jobs in the long run, as indicated by student debt statistics.

Source: NBC News

A US College Board study has indicated that the average debt was of $26,900 in 2017, for students graduating public 4-year schools

Therefore, we can easily spot a constant fluctuation of the average values. Any future student must take this aspect carefully into account. It is often recommended for students to have a source of income during their college years, since failure to do so generally entails racking up credit card debt on-top, according to student loan debt statistics.

Source: CNBC

A research effort has concluded that graduates of non-profit 4-year private schools generally have to pay $32,600 in student debt

Based on this, we can determine that non-profit private schools are considerably more expensive than public, state-owned universities. Similarly, it is also important to mention that debt is even higher for graduates of for-profit private universities, where tuition rates tend to skyrocket.

Source: CNBC

States with the Highest Student Loan Debt

A study that was conducted in 2019 has managed to determine the states with the highest student loan debt on average. Here are the results:

| State | Average Debt for Students |

| DC | To answer the question “what is the average student loan debt here”, we must mention that it is approximated at $55,279. Seeing how DC is home to some top-ranking universities in the US, it only makes sense that it ranks first. |

| Georgia | As part of this chart, Pennsylvania classes second, granted that it has an average of $40,962. This data is provided by an Experian study. |

| Maryland | Maryland classes just below Georgia, thanks to its $40,630 average student loan. |

| New York | New York is the fourth state in terms of the highest average student debts. As such, the numbers are estimated at $37,753. |

| California | Last but not least, our list ends with California, where the debt is approximated at $37,468. |

Source: Experian

States with the Lowest College Debt

A study that was conducted in 2019 has managed to determine the states with the lowest student loan debt on average. Here are the results:

| State | Average Debt for Students |

| South Dakota | Reports indicate that South Dakota represents the state where students can generally expect the lowest amount of student loan debt. With this in mind, research efforts point out that the average college student debt here is around $28,782. |

| Wyoming | The second state in terms of the lowest average is Wyoming. Here, the debts are estimated at $28,974, thus being considerably lower when compared to the states on the higher end of the chart. |

| North Dakota | Those looking to study in North Dakota will also be pleased to see that debts are generally lower here as well. The average here is around $29,267. |

| Iowa | Iowa is a bit more expensive, granted that the average debt is only $29,416. |

| Nebraska | Despite the more expensive lifestyle in Nebraska, the average amount of student loan debt is low here as well. The average debt here is around $30,013. |

Source: Experian

Stats for Student Loan Debt by Program and Type

At this point, the interest rate of student loans is the lowest in the case of direct subsidized loans for undergraduates

As such, the debt rate between 2018 and 2019 is estimated to sit at 5.05%, which is the lowest of them all. Unfortunately, the rate has increased over the last couple of years, given that average student loan payment stats indicated an interest rate of 3.76% in 2016–2017. The same numbers are applicable to direct unsubsidized loans for undergraduates.

Source: Debt

In the case of direct unsubsidized loans for graduates, the interest rate in 2018–2019 was approximated at 6.60%

As such, graduates looking to further expand their area of knowledge can expect to pay a higher interest rate for their loans. The rate has also increased with time, given that it was estimated to sit at 5.31% during 2016–2017, according to the average student loan debt 2017 stats.

Source: Debt

The highest interest rates are present with Direct PLUS loans given for graduates and parents

Studies have concluded that the average interest rate for these loans is situated at 7.60% annually this year. The rate has increased with time, given that it was sitting at 6.31% annually during 2016–2017.

Source: Debt

In 2007 and 2008, the FFEL student loan program served a total of 6.5 million students, lending approximately $54.7 billion worth of loans

Back then, the program was responsible for issuing 80% of federal student loans. It is important to point out that the program was terminated in 2010, likely being one of the main reasons why the average college student loan debt has increased so considerably. It is essential for the US Federal Government to kick-start more programs meant to reduce the number of loans for students, ensuring that US-based students have equal opportunities at getting a quality higher education. Failure to do so will likely lead to these numbers piling up, thus creating an actual crisis in the US university system.

Source: US Department of Education

Average Student Loan Debt by Age

Considerably more people aged 60 and older are now dealing with student loan debt

Estimates showcase that the overall student loan debt for people aged 60 and older has increased by roughly 1256% from the 2004 numbers. Back then, there were only $6.3 billion owed by people in this age bracket. In 2017, $85.4 billion were owed.

Source: ValuePenguin

Borrowers who are between 30 and 39 generally have the highest amount of student debt, when compared to individuals included in other age brackets

As such, this student loan debt fact does showcase that people of this age generally have a harder time dealing with all of the debt that has piled up. This aspect is most likely related to the fact that people tend to spend the most at this age since many are buying houses, building their families, and having children.

Source: ValuePenguin

Since 2004, age statistics indicate that most student loan debtors were aged 30 and under

The numbers remain consistent throughout the last decade, and up to 2018 when the statistic was published. It is very likely that the numbers remain similar today. As such, borrowers between 20 and 30 years of age currently owe 65% of the total student loan debt in the United States, according to the average student loan debt 2018 data.

Source: ValuePenguin

Here are the numbers depicting student loan debt values, based on age groups:

- Individuals aged below 30 years of age owed $383.8 billion in 2017.

- Individuals in the 30–39 age bracket owed $461 billion.

- Those aged between 40 and 49 owed $278.9 billion.

- People aged 50 to 59 were estimated to owe $177.2 billion.

- Last but not least, those aged 60 and over owed $85.4 billion.

Source: ValuePenguin

Distribution of Total Student Loan Debt by Balance

In 2017, it was estimated that 8.54 million people owed less than $5,000

Based on this statistic, we can conclude that numerous US graduates are close to paying their debt off completely. It is likely that these individuals have been paying off their loans for several years.

Source: ValuePenguin

12.27 million US residents have withstanding loans ranging between $10,000 and $25,000

This distribution statistic showcases that people owing this balance are the most numerous at this point. They are closely followed by people owing between $25,000 and $50,000, since 8.6 million loans exist here, as indicated by student loan statistics. These numbers are bound to increase in the next couple of years, as more US residents wish to enroll in a university.

Source: ValuePenguin

609,800 people owed more than $200,000-worth of student loan debts in 2017

A similar amount of people owe debt situated between the $150,000 and $200,000 threshold. Generally, these are people who went to for-profit private universities.

Source: ValuePenguin

How College Type Affects Average Student Debt

For-profit educational institutions are known for receiving 90% of their total revenue from federal student aid

Generally, these institutions have high tuition costs, since their main purpose is to get higher amounts of profit. This is also why numerous students attending such institutions tend to request federal college aid.

Source: National Association for College Admission Counselling

Non-profit educational institutions are generally cheaper when compared to profit-based institutions, leading to lower average student debt

As such, it is important to mention that most US-based non-profit universities receive their funding from tuition, endowments, and local governments. What makes them special is the fact that this capital is re-invested into college operations, such as the curriculum and facilities for students.

Source: My College Guide

The actual average for student debt also depends on whether a college is public or private

Public colleges are state-owned, which means they generally have lower tuition fees. Generally speaking, there is a rumor on the education market that private colleges offer better education and facilities, although this can depend on several factors, according to student debt statistics. Lower rates are offered for state residents in the case of public colleges.

Source: My College Guide

According to a report released by the Centre on Education statistics, graduation rates for bachelor’s degrees are situated at 42% at for-profit institutions, 57% at public schools, and 65% at private non-profit universities

Based on this, we can conclude that the actual quality of education, alongside the price of tuition, depends from case-to-case. Therefore, before enrolling in university, it is essential for future students to carry out their due diligence, to ensure they’re making the best choice from both a monetary (college debts), and a quality-of-education perspective.

Source: My College Guide

In 2012, graduates of colleges that are for-profit had debts estimated to be 45% higher when compared to other schools

Despite the higher revenue for these colleges, most of the tuition isn’t reinvested into facilities and the curriculum, thus leading to the questionable quality of education despite the higher price. However, university centers with prestige generally strive to maintain it.

Source: Finder

How the Program Affects the Average Student Debt

IT-centered Universities tend to attract the highest amount of student loan debt in the United States

According to a report published by Finder, the highest debt is accumulated from technology-based institutes. Relevant examples include the Wentworth Institute of Technology and the Stevens Institute of Technology, where the average undergraduate student loan debts are $59,000, and $51,000 respectively.

Source: Finder

Law school students in the United States generally graduate with an average debt of $145,550

This includes undergraduate loans and is based on data released by the National Centre for Education Statistics. Therefore, anyone looking to become a lawyer should expect massive amounts of debt. Paying this debt back is easier when compared to other programs, according to student debt statistics, due to high lawyer salaries.

Source: Nerd Wallet

In 2011, the average debt for medical graduates was estimated at $173,000

Future doctors must ensure funding during their college years to make paying this debt easier. As with law school, graduates are often given higher-paying jobs — hence why clearing the overall debt is significantly easier.

Source: Student Debt Relief

In the US, Ph.D. graduates owe roughly $98,000 in average student debts

It is important to point out that the high value here is also based on the fact that numerous Ph.D. graduates had withstanding loans from previous educational programs. Therefore, the actual tuition costs for a Ph.D. degree leads to lower debt when considered exclusively.

Source: CNBC

Students participating in Master’s degrees borrowed approximately $18,210 per year during 2015

On the other hand, it is important to mention that during the same year, undergraduates borrowed roughly $5,460 annually, which is considerably less, as outlined by the US Chamber of Commerce.

Source: US Chamber of Commerce

College Debt Statistics by Gender

A DEBT study has concluded that 62% of college graduates are likely to take credit card loans, followed by 37% of those who haven’t graduated high school, followed by 31% of those in college, and 23% of those still in high school

Therefore, credit card debt is most often taken by college graduates, in an effort to support their lifestyle, while also being able to slowly pay back college debt.

Source: DEBT

Women need more time to pay off their college student debts

A study made by the Chamber of Commerce highlighted that women often struggle for longer when it comes to paying off their student loan debt. One argument could be the gender pay gap, given that women make 26% less money compared to their male counterparts. Similarly, women hold roughly 2/3 of the total student-related debt.

Source: Chamber of Commerce

According to a report issued by the American Association of University Women, upon graduating, women have $2,700 more student debt

The reasons behind this spike are currently unknown. Still, women are generally believed to spend more on education compared to men.

Source: Business Insider

Student Loan Forgiveness Statistics

In 2019, 90,962 unique student borrowers have submitted public service loan forgiveness applications

The same data source indicates that $52 million represents the total balance that has been discharged from borrowers with an approved application; many of these applications are actually rejected.

Source: Student Aid

In 2017, roughly 550,000 borrowers were expected to have their student loan debts forgiven

These are promising stats, yet there’s still lots of work to be done on this matter.

Source: Student Aid

Conclusion

Based on everything that has been outlined thus far, over $1.5 trillion worth of student debt was owed during 2018; a massive number, proving that the US higher education system is in desperate need of reform. The student loan default rate was over 21% for white students and 50% for black, between 2003 and 2015. Likewise, it often takes students around 20 years to pay back their loans completely, making their financial situation unsteady for years on end. We can also spot the big difference when comparing college programs and types, therefore no standardized approach for student loan debt is available at this point.

Last but not least, we hope that our student loan debt statistics will help paint a clearer picture of the higher education system in the United States, encouraging others to push for reform, while also aiding students when gauging their expected debt.

{kind=link}